Exhibit 1: By CY22 end, we saw a median -30% decline of leading IPOs of 2021

1758105929942.jpg)

Source: Ambit Asset Management, chittorgarh.com

While this recent rally might be backed by underlying fundamentals of the economy improving significantly and in the hope of stabilizing global macros, the extent and quantum of it, however, in addition to 2-3 other important factors – which we highlight in this report – warrant attention and perhaps caution. In this note, we take a look at these factors, compare them to earlier cycles, and try to understand where we are headed.

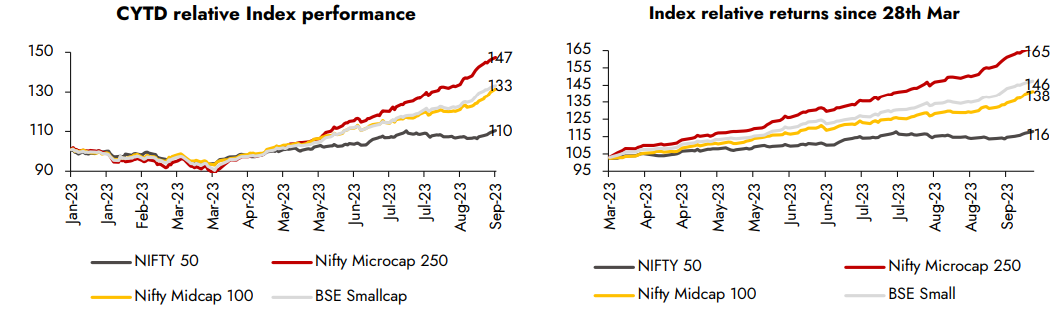

Exhibit 2: Broader markets have outperformed NIFTY in CY23… Exhibit 3: …Especially post the Regional Bank crisis in the US

Source: Ambit Asset Management, ACE Equity, Till 11th Sep 2023

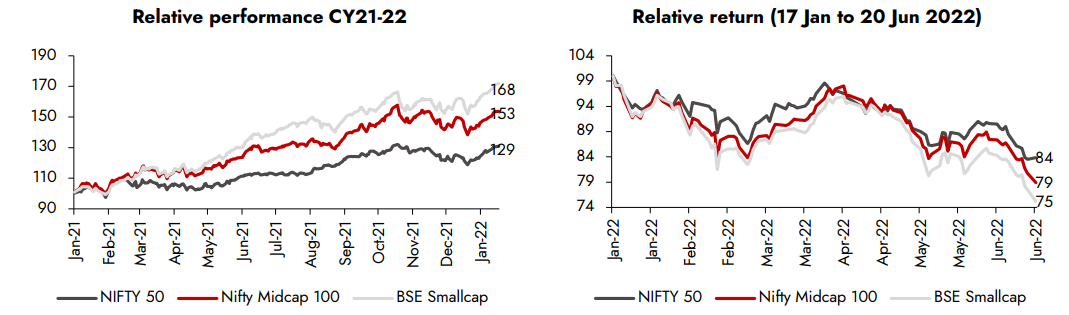

Exhibit 4: A similar trend was seen in CY21… Exhibit 5: …which followed a sharp correction as the narrative weakened

|

Source: Ambit Asset Management, ACE Equity |

Beyond Euphoria!

- Bunch of selling by insiders (Promoters / strategic investors) – CY23 for markets also stands out from the perspective of promoters and strategic investors (Private Equity) stake sale. These are the people who know the underlying business the best. Promoter selling in CYTD23 stood at Rs807bn which is ~2x from CY22 and ~50% higher from the earlier peak in CY20 (Refer Exhibit: 6). Many of the companies where promoters or strategic investors were looking for an exit (as per media articles) have taken place in quick succession over the last few months (Refer Exhibit: 7, 8). The bunching-in of these transactions over such a short duration may indicate fair market liquidity and valuations, at least over the near term.

Exhibit 6: Selling by insiders in India Inc. has already surpassed the earlier peak

1758105965975.jpg)

Source: Ambit Asset Management, CNBC TV18, *Till 18th Aug-2023

Exhibit 7: Slew of bulk deals have taken place, especially over the last month

1758105973748.jpg) Source: Ambit Asset Management, BSE Note: Data includes only SELL transactions to avoid duplications. Only large deals are considered hence list is not exhaustive. * - Data till 6th Sept 2023

Source: Ambit Asset Management, BSE Note: Data includes only SELL transactions to avoid duplications. Only large deals are considered hence list is not exhaustive. * - Data till 6th Sept 2023

Exhibit 8: A lot of large stake sale/divestments by promoters/large investors over the last few months

1758106011793.jpg)

Source: Ambit Asset Management, NSE, BSE, As of 6th Sep 2023

2. Increased Retail fund flow toward riskier categories – In addition to the above, retail investors’ fund flow is increasingly gravitating toward riskier segments. Mainboard IPOs are being heavily over-subscribed, the number of SME IPOs has seen a sharp jump over the last few years (Refer Exhibit: 10), and Mutual Funds are seeing increased flow in Small/Mid Caps in place of large-caps (Refer Exhibit: 9). While this may very well be an indication of increased market participation and financialization of savings, the quantum of it when studied in retrospect with past market cycles warrants attention.

Exhibit 9: Sharp uptick in Small/Mid cap fund flows in contrast to Large Cap funds Net Monthly MF Inflow is still below H1CY22 peak

1758008028515.jpg)

Source: Ambit Asset Management, AMFI Data

Exhibit 10: SME IPOs are crossing earlier peak in terms of no. and size of issues

1758106038350.jpg)

Source: Ambit Asset Management, chittorgarh.com, Note: NSE and BSE SME IPOs

Exhibit 11: Increased F&O participation + new contract addition = increased speculation ratio on

1758106044103.jpg)

Source: Ambit Asset Management, I-Sec Research, WFE, Note: Data of leading exchange(s) across these countries

3. PSUs, Cap goods and Manufacturing industries have seen the sharpest run-up – absolute and relative – Among the top performers in BSE-500 index constituents, the majority have been in the Cap Goods, Manufacturing, or PSU / Defense theme which has caught on to the investor frenzy. Defense, Make-in-India, and pre-election spending by the government have led to buoyant order flows in the construction/engineering space.

Exhibit 12: BSE-500 top performers from the lows of 28th March – Infra/Construction/Manufacturing stands out

1758106059114.jpg)

Source: Ambit Asset Management, ACE Equity

4. Quality is paramount! – What should we as investors do in such a scenario? This is a question we often get asked. We would like to emphasize the importance of sticking with companies with strong ‘Earnings’ potential (Refer Exhibit: 15) AND ‘Quality’ (Corporate governance, Capital allocation, low Debt). This is the core to our ‘Good & Clean’ approach to portfolio construction, especially for Mid / Small Caps. While such a strategy might underperform periodically during times of extreme optimism (Euphoria), it has consistently helped protect downside during tough periods (Refer Exhibit: 13, 14). Thus, over a longer term, the point-to-point returns out-perform the index by a fair margin.

Exhibit 13: Our Midcap portfolio performed well during sharp market correction…

1758106067389.jpg)

Source: Ambit Asset Management, Note: *BSE 500 TRI is the selected benchmark for the Ambit Good & Clean Midcap. The same is reported to SEBI. Nifty Midcap100 was the benchmark in CY18 and CY19

Exhibit 14: … similar to our Small-Cap Portfolio

1758106074970.jpg)

Source: Ambit Asset Management, Note: *BSE 500 TRI is the selected benchmark for Ambit Emerging Giants. The same is reported to SEBI. Nifty BSE Small Cap Index was the benchmark in CY18 and CY19

Exhibit 15: It is ‘Earnings’ which is the eventual ‘fuel’ to stock price movement, as can be seen over the longer duration in SmallCap Index, companies with the strongest earnings momentum have outperformed the most

Source: Bloomberg, Ambit Capital research

Conclusion

While the recent market rally may have come as a huge relief for the investors after an 18-month-long sideways movement, there are enough reasons to believe that caution is warranted and that it may well be foolhardy to believe that the current rally will not witness a pullback. Insiders such as promoters or strategic investors are the ones who know the most about a specific business. We see them buy when prices are depressed and sell when the overvaluation kicks in to realize some gains. The bunch-up of these in the past few months in addition to the increased small/micro-cap run-up warrants attention. We remain confident about the India story in the medium to long term and believe we are on track to touch the $10tn mark over the next decade. We continue to emphasize our philosophy of ‘Good & Clean’ especially in Small/Mid-Caps with focus on ‘Earnings’ growth and ‘Quality’ management. We feel that short-term volatility may persist as we head into elections. Over the long run, however, we expect the markets to be fundamentally driven.